Abstract: I consider legal decisions resulting in the end of the Federal Communications Commission’s net neutrality regulation. There is evidence that net neutrality regulation has diminished incentives to invest in internet access and increased transaction costs in the market for access. As a result, net neutrality regulation may have constrained e-commerce. I conclude that ending net neutrality regulation may increase investment in internet access and enhance the development of e-commerce.

***

1. Introduction

Ohio Telecom freed internet access from the tangle of net neutrality regulations.[1] With the end of Chevron deference to administrative agencies, the courts could evaluate the regulation of fixed and mobile internet access. Ohio Telecom lifted the Federal Communications Commission’s (FCC) internet access restrictions. I review the events that led to the end of net neutrality regulation. I consider how a quarter of a century of sporadic net neutrality regulation impacted internet access and e-commerce, which has reached only 16% of retail sales. I argue that the end of net neutrality regulation should promote internet usage and stimulate the growth and development of e-commerce.

Internet access is critical for the development of e-commerce. According to Ohio Telecom, “[b]roadband is the Internet’s lynchpin. It enables our access to and usage of the Internet, acting as an international superhighway that rapidly transports requests for and receipt of electronic data from one point to another and back again.”[2] The Court of Appeals noted “[w]hether from a push of a button on a computer, a smart TV remote, or a virtual keyboard on a mobile device, consumers instantly, reliably, and seamlessly experience the Internet thanks to Broadband Internet Service Providers like Spectrum, Xfinity, and AT&T Internet.”[3]

Internet access regulation by the FCC was inconsistent and generated uncertainty. Ohio Telecom observed that “[b]eginning in the late 2000s, the FCC undertook several attempts to impose so-called ‘net neutrality policies,’ which prohibit Broadband Internet Service Providers from controlling users’ Internet access—by varying speeds or blocking connections to third-party websites, for example—based on content, commercial agreements, and other reasons a provider might want to manage a user’s Internet experience.”[4] As Ohio Telecom notes, the FCC’s “efforts culminated in 2015, when the FCC concluded for the first time that Broadband Internet Service Providers offer to consumers a ‘telecommunications service’ and thus are common carriers — and subject to extensive regulation (including net-neutrality restrictions) — under Title II of the Communications Act.”[5] Then, in 2018, the FCC removed these regulations and “reverted to its historical hands-off approach to Internet regulation by concluding that Broadband Internet Service Providers offered only ‘information service’.”[6]

Finally, in 2024, the FCC resumed what Ohio Telecom called its “heavy-handed regulatory regime” under the net neutrality banner.[7] In its net neutrality ruling, the FCC stated “[t]oday, we reclassify broadband Internet access service (BIAS) — the consumer broadband service that we use and rely on every day — as a telecommunications service under Title II of the Communications Act of 1934, as amended (the Act).”[8]

I apply a general framework for evaluating various types of internet access. I argue that net neutrality regulation distorted prices and decreased efficiency in the market for internet access. I point out that market demand for internet access is a derived demand because it depends on demand for final services such as e-commerce, social media, entertainment, information, communication, and artificial intelligence (AI). The analysis concludes that the end of net neutrality regulation improves the prospects for the development of the digital economy.

2. From Chevron Deference to Ohio Telecom

Internet providers and users faced on-again-off-again net neutrality regulation for about twenty-five years. Early on, the FCC imposed a patchwork of regulations that differentiated between Internet provision through coaxial cable and telecommunications. The FCC’s net neutrality ruling in 2024 created significant regulatory burdens before being removed by Ohio Telecomm. This section traces some of the legal developments leading to the end of net neutrality regulation.

I began to study the economics of regulation before Chevron. Later, in Regulation and Markets, I addressed the relationship between economic regulation and administrative process.[9] I observed that most regulatory agencies “have extensive powers and significant latitude in formulating policy and independence of action.”[10] I cited a 1937 president’s commission that referred to independent regulatory agencies as a “headless ‘fourth branch’ of the Government, a haphazard deposit of irresponsible agencies and uncoordinated powers.”[11] I noted that agencies needed to be accountable to Congress and the Executive, and at the same time, “it is desired that regulatory agencies proceed fairly, that they accord individuals the due process of law, and that their decisions are consistent with judicial review.”[12] I suggested that “[u]nfortunately, achieving these two purposes within any single agency may be inconsistent or problematic at best.”[13]

Independent regulatory agencies conflict with the constitutional separation of powers and the system of checks and balances. The Supreme Court’s Chevron decision only worsened the problem of independent agencies.[14] Chevron involved a regulation issued by the Environmental Protection Agency (EPA). Chevron considered “whether EPA’s decision to allow States to treat all of the pollution-emitting devices within the same industrial grouping as though they were encased within a single ‘bubble’ is based on a reasonable construction of the statutory term ‘stationary source’.”[15]

According to Chevron, “if the intent of Congress is clear, that is the end of the matter; for the court, as well as the agency, must give effect to the unambiguously expressed intent of Congress.”[16] The decision added that if “Congress has not directly addressed the precise question at issue, the court does not simply impose its own construction on the statute, as would be necessary in the absence of an administrative interpretation. Rather, if the statute is silent or ambiguous with respect to the specific issue, the question for the court is whether the agency’s answer is based on a permissible construction of the statute.”[17]

The Supreme Court in Chevron stated that it had “long recognized that considerable weight should be accorded to an executive department’s construction of a statutory scheme it is entrusted to administer, and the principle of deference to administrative interpretations.”[18] Chevron ruled that “the Administrator’s interpretation represents a reasonable accommodation of manifestly competing interests and is entitled to deference: the regulatory scheme is technical and complex, the agency considered the matter in a detailed and reasoned fashion, and the decision involves reconciling conflicting policies.”[19]

The Supreme Court in Brand X relied on Chevron deference to uphold the FCC’s different treatment of Internet Service Providers (ISPs) depending on whether access came through cable modems or telecommunications.[20] In Brand X, the Court upheld the FCC’s classification of cable modems as an information service rather than a telecommunications service. The Court reasoned that internet access was a bundle of information services and telecommunications components. Justice Antonin Scalia foresaw the problems such deference would create, observing in dissent that “[e]ven when the agency itself is party to the case in which the Court construes a statute, the agency will be able to disregard that construction and seek Chevron deference for its contrary construction the next time around.”[21] Scalia observes that the FCC “has once again attempted to concoct ‘a whole new regime of regulation (or of free-market competition)’ under the guise of statutory construction.”[22]

The landmark Loper Bright decision concerned a very different kind of net – fisheries regulation by the National Marine Fisheries Service (NMFS).[23] Loper Bright overturned “Chevron deference”, changing the entire regulatory landscape. Chief Justice Roberts noted that since Chevron, the Supreme Court “sometimes required courts to defer to ‘permissible’ agency interpretations of the statutes those agencies administer—even when a reviewing court reads the statute differently. In these cases, we consider whether that doctrine should be overruled.”[24] In overruling Chevron, the Supreme Court stated “[c]ourts must exercise their independent judgment in deciding whether an agency has acted within its statutory authority, as the APA [Administrative Procedures Act] requires.” Although Roberts noted the relevance of Executive Branch judgement and Congressional delegation to an administrative agency, he cautioned that “courts need not and under the APA may not defer to an agency interpretation of the law simply because a statute is ambiguous.”[25]

Loper Bright set the stage for Ohio Telecom by removing the courts’ deference to regulatory agencies. This allowed the court to review the FCC’s net neutrality ruling. In designating Internet access as an “information service”, Ohio Telecomcited the definition in the US code: “the offering of a capability for generating, acquiring, storing, transforming, processing, retrieving, utilizing, or making available information via telecommunications, and includes electronic publishing, but does not include any use of any such capability for the management, control, or operation of a telecommunications system or the management of a telecommunications service.”[26]

Ohio Telecom removed net neutrality regulation from fixed broadband access. Ohio Telecom held “that Broadband Internet Service Providers offer an information service and that mobile broadband is a private mobile service. Therefore, the FCC exceeded its statutory authority by issuing the Safeguarding Order.”[27] According to Ohio Telecom, “[b]roadband Internet Service Providers offer consumers the capability to acquire, store, and utilize data—and thus offer consumers an information service.”[28]

Ohio Telecom extended deregulation to mobile broadband access. The Ohio Telecom decision pointed out that “[i]n 1993, Congress added a ‘mobile services’ provision to the radio-transmission part of the Communications Act (Title III).”[29] The Court of Appeals concluded that mobile broadband is an information service that should not be regulated as a commercial service. The decision removed net neutrality restrictions from the critical area of mobile commerce.

Net neutrality regulation continues in some states. Bryan Veney observes that “California’s SB-822, the most comprehensive state net neutrality law, bans blocking, throttling, and paid prioritization.[30] Washington, Oregon, Colorado, and Vermont also have net neutrality regulations for residential internet access.[31] New York, New Jersey, and Maine enforce net neutrality regulations through state procurement contracts or executive orders.[32]

3. Internet Access and Net Neutrality Regulation

This section considers how internet access and e-commerce fared under FCC regulation. I apply a general framework to examine the effects of net neutrality regulation. Then, I review evidence on the effects of net neutrality regulation on internet access. I suggest that such restrictions may have limited the development of e-commerce.

Daniel Spulber and Christopher Yoo identified five categories of internet access: (1) retail access, (2) wholesale access, (3) interconnection access, (4) platform access, and (5) unbundled access.[33] These types of access refer to the recipient of internet access. Thus, a network provides retail access to consumers and firms who are end users. A network provides wholesale access to resellers of the network’s services. A network provides interconnection access through reciprocal agreements with other networks. A network provides a platform for firms supplying complementary products to the network’s customers. Finally, a network provides unbundled access to competing firms that use some of the network’s inputs.

Applying this framework, Spulber and Yoo found that the regulation of internet access, such as net neutrality rules, necessarily limits market alternatives. This is because firms that provide networks and access services choose a mixture of vertical integration and market contracts by comparing organizational and transaction costs. This is closely related to Ronald Coase’s analysis of the nature of the firm.

The FCC’s 2024 net neutrality ruling focused on regulation of retail and wholesale access.[34] However, the ruling also regulated unbundled access.[35] The ruling also included some platform access: “[w]e find that DNS [Domain Name System], caching, and other services the BIAS providers use with their BIAS offering comfortably fit within the telecommunications systems management exception, either because they are used to manage a telecommunications service; used to manage, control, or operate a telecommunications system; or both.”[36] The FCC claimed forbearance for interconnection only because it had regulatory authority elsewhere.[37]

The FCC’s 2024 net neutrality ruling indirectly affected all types of internet access because regulation-induced price distortions for one type of access will change network configurations and market contracts. Classifying retail access as a telecommunications service rather than an information service thus affected transactions involving the other types of access.

In contrast, allowing network diversity allows competition to find the most efficient market contracts and network designs.[38] Network diversity benefits consumers by allowing product variety. Network diversity also benefits consumers because it relies on market participants to determine access contracts, which lowers transaction costs and decreases prices.

Network diversity, rather than net neutrality, offers a better guide for regulation, as explained by Daniel Spulber and Christopher Yoo in Networks in Telecommunications.[39] By promoting network diversity, regulation increases competition and product variety in internet access. Network diversity provides incentives for internet access providers to offer innovative forms of access such as mobile broadband. Diversity in network access allows multiple internet access providers to serve the market with differentiated products and technological alternatives.

Net neutrality regulation diminishes incentives to invest by access providers. In contrast, product variety in internet access increases incentives for investment. Matthew Lesh pointed out “[i]n most markets, from airline tickets to grocery shopping, consumers can choose from a multitude of options. This variety is in the consumers’ interest as it allows varied preferences to be fulfilled. Yet when it comes to the internet, ISPs must all provide full and indiscriminate access, competing almost entirely on price and speed.”[40] Lesh adds that “[t]here is evidence that net neutrality reduces investment in telecommunications infrastructure. In addition to harming consumers, this undermines the government’s gigabit broadband and ‘levelling up’ goals.”[41]

Net neutrality regulations are likely to have high compliance costs and diminish economic efficiency by distorting market decisions. The economics literature provides little evidence that such regulations will create economic benefits. The likelihood of substantial costs and the absence of benefits suggest the need for regulatory forbearance.

The academic literature on net neutrality spans a number of disciplines, including economics, law, management, and information systems.[42] Wolfgang Briglauer and Christopher Yoo survey the literature and note “[t]he lack of clear evidence of net neutrality’s consequences for the main economic actors in the Internet ecosystem – content providers (CPs), ISPs, and consumers/end users – makes it all but impossible to assess whether the intervention creates benefits sufficient to justify the high implementation, monitoring, and enforcement costs that net neutrality entails.” [43]

Shane Greenstein et al. survey the economics literature related to network neutrality, focusing on complementary inputs, vertical relationships, and market power of ISPs.[44] They observe “[t]he most basic definition of net neutrality is to prohibit payments from content providers to internet service providers; this situation we refer to as a one-sided pricing model, in contrast with a two-sided pricing model in which such payments are permitted.”[45] They also note that “[n]et neutrality may also be defined as prohibiting prioritization of traffic, with or without compensation.”[46] According to Greenstein et al., who advocate regulatory restraint: “the thrust of the conclusions from economic analysis tilt against simplistic declarations in favor or against net neutrality. This suggests that bold and sweeping recommendations and interventions, given the current state of empirical knowledge, have a substantial chance of being misguided.”[47]

Barbara Van Schewick uses a narrow definition of network neutrality as “non-discrimination rules that forbid operators of broadband networks to discriminate against third-party applications, content or portals (‘independent applications’) and to exclude them from their network.”[48] Van Schewick recognizes that there are regulatory costs in terms of both investment and innovation: “[a]part from creating the costs of regulation itself, network neutrality rules reduce network providers’ incentives to innovate at the network level and to deploy network infrastructure.”[49] Van Schewick’s arguments for net neutrality rules rest on a network provider satisfying exceptions to the one-monopoly-rent theorem. Van Schewick presents little or no empirical evidence that monopolizing a complementary market has occurred. Van Schewick gives the example of the FCC’s statement in the AOL/Time Warner merger that “’[t]he record in this proceeding provides some evidence that AOL already seeks to limit its members’ access to unaffiliated content on the World Wide Web. For example, AOL requires that content appearing on AOL websites have only a limited number of hyperlinks to unaffiliated content.”[50] But the AOL/Time Warner merger contradicts this argument. AOL acquired Time Warner “for $182 billion (which is $332 billion in inflation-adjusted dollars today),” but resulted in “the worst business deal in history.”[51]

An empirical analysis of regulatory effects on capital investment conducted by George Ford found that “[a] revival of prescriptive regulation of telecommunications services in the United States beginning in 2010 – following two decades of an active deregulatory agenda – had firms, financial analysts, and even regulators fearing reduced capital spending by service providers on Internet networks as a consequence.”[52]

Although net neutrality has ended in the US, it remains in force in the EU (Reg (EU) 2015/2120), in India (TRAI 2018), and across several Latin American jurisdictions. There is evidence in the EU that net neutrality regulation diminished incentives to invest in internet access. Wolfgang Briglauer et al. provided an empirical analysis of the effects of net neutrality regulation for countries in the Organization for Economic Cooperation and Development (OECD).[53] They applied “a comprehensive and most recent OECD panel data set for 32 countries for the period from 2000 to 2021 covering the entire high-speed broadband network deployment period.”[54] They found that “imposing strict net neutrality regulations clearly slow down the deployment of new fiber-based broadband connections.”[55] Adam Rennhoff and James Bakuli, compared “outcomes for 10 states that retained state-level net neutrality rules following the Federal Communications Commission’s national repeal of net neutrality rules in 2018.”[56] They found “that the number of ISPs increased more in states without net neutrality regulations.”[57]

The market for broadband internet service became highly concentrated under net neutrality regulation. According to the American Society of Civil Engineers 2025 Report Card, “[t]he FCC’s June 2024 broadband map shows that 94% of U.S. households can access a broadband connection at home that meets the FCC’s high-speed internet definition.”[58] The 2025 Report found that “[a]lmost 3,000 internet service providers (ISP) exist in the U.S., yet the bulk of broadband service is delivered by a few large, private ISPs. Homes and businesses connect via wired or wireless connections, with numerous technologies delivering services described under the umbrella term broadband.”[59]

Scott Wallsten and Stephanie Hausladen examine the international net neutrality debate.[60] They observe that “European countries, and the EU in particular, tend to focus on competition between Internet Service Providers (ISPs) providing DSL service over an infrastructure operator’s (generally the incumbent’s) wires – or intra-platform competition. Consistent with this view, the E.U. has promoted various types of unbundling policies, in which the infrastructure owner must allow competing ISPs to offer services over its lines.”[61] Wallsten and Hausladen find that “countries with more broadband connections per capita provided through local loop or bitstream unbundling have fewer fiber connections and WLL [Wirelesss Local Loop] per capita provided by the incumbent and entrants.”[62] They also find “countries that rely more on unbundled lines to provide broadband see less investment by incumbents in fiber than countries that rely less on unbundled lines and more on facilities-based entry.”[63]

4. Net Neutrality and E-Commerce

Determining the economic effects of net neutrality regulation should focus on the benefits and costs to consumers and firms that use the internet. The demand for internet access and internet transmission is a derived demand that depends on the underlying benefits and costs of using the internet. The availability and costs of internet access will affect the usage of the internet, including e-commerce. Policy discussions and academic research on the effects of net neutrality regulations have tended to miss the mark by focusing on ISPs. The emphasis on access neglects regulatory effects on the usage of the internet, including e-commerce.

Internet access is only one of a number of factors that affect the adoption of e-commerce. There are transaction costs of using e-commerce, even though digital technologies have lowered these costs.[64] Also, e-commerce faces competition from traditional brick-and-mortar channels.[65] Omnichannel marketing has integrated e-commerce and brick-and-mortar channels, taking advantage of complementarities among channels.[66] These factors and other market forces make it difficult to identify the effects of net neutrality regulation on e-commerce.

The FCC’s net neutrality ruling did not consider the connection between Internet access and e-commerce. The FCC argued against comparisons between broadband investment and investment in other industries such as transportation and warehousing. The FCC suggested that the effects of net neutrality regulation on telecom investment had little to do with e-commerce: “[i]nvestment in transportation and warehousing rose dramatically during the post-2010 time period due to the boom in e-commerce that occurred. This trend makes this industry a poor choice for predicting what the trend in telecommunications investment would have been absent the announcement of the potential for BIAS to be reclassified as a Title II service.”[67]

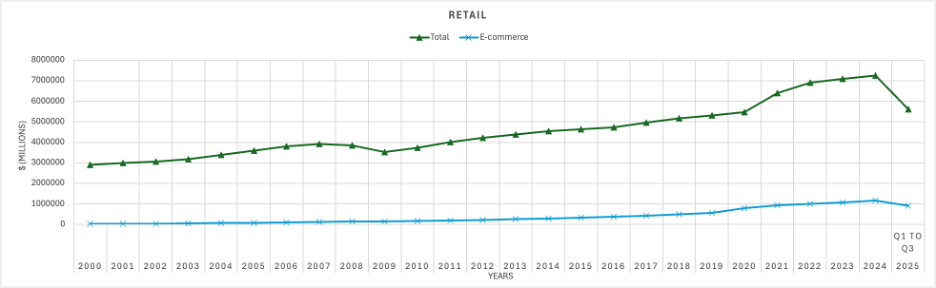

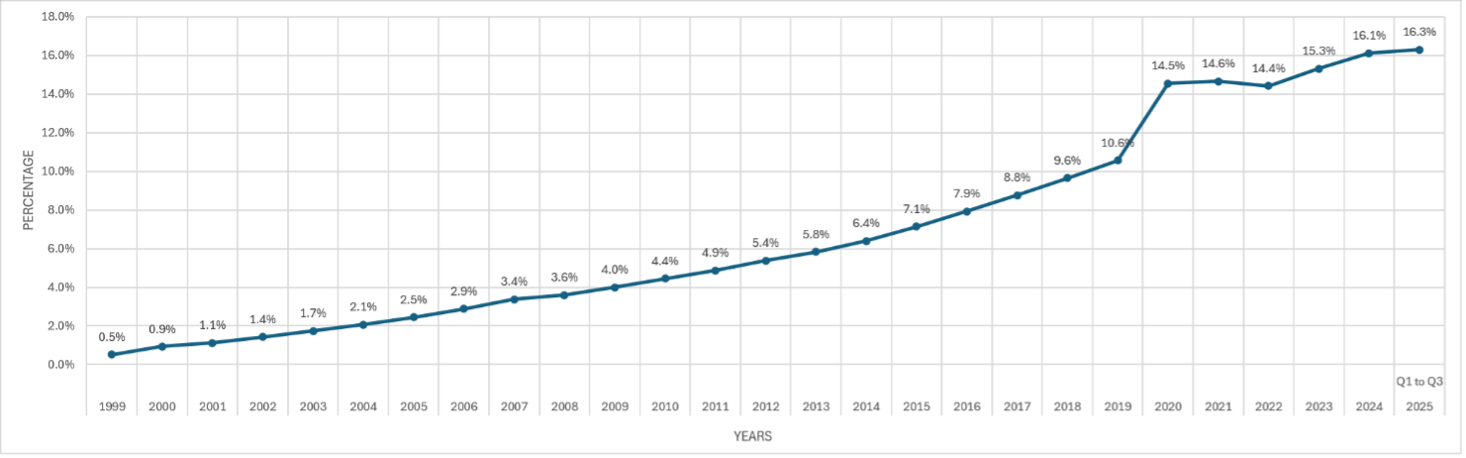

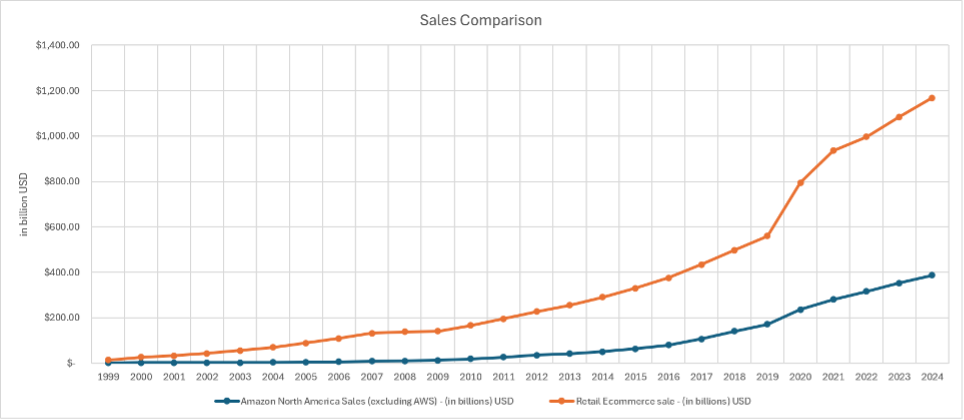

Sporadic net neutrality regulation coincided with e-commerce only attaining a small share of retail sales. Observing the usage of the internet provides some indication of the effects of net neutrality regulations on internet access. Most concerning is the usage of the internet for e-commerce. In comparison with retail sales, retail e-commerce experienced limited growth during the relevant twenty-five-year period. Figures 1a and 1b show that retail e-commerce reached only 16% of retail sales. A significant portion of e-commerce was provided by just one company. Figure 2 compares Amazon’s North American retail sales, excluding Amazon Web Services (AWS), with U.S. e-commerce. Without Amazon, e-commerce is a much smaller share of retail transactions.

Figure 1a: Retail E-commerce sales versus Total Retail sales

Figure 1b: Retail e-commerce as a percentage of Total Retail sales[68]

Figure 2 Comparison of U.S e-commerce retail sales with Amazon’s North American retail sales, excluding Amazon Web Services (AWS)[69]

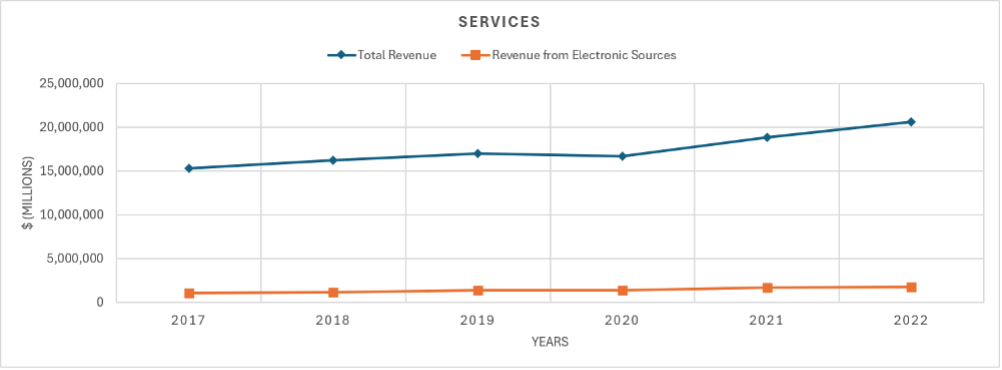

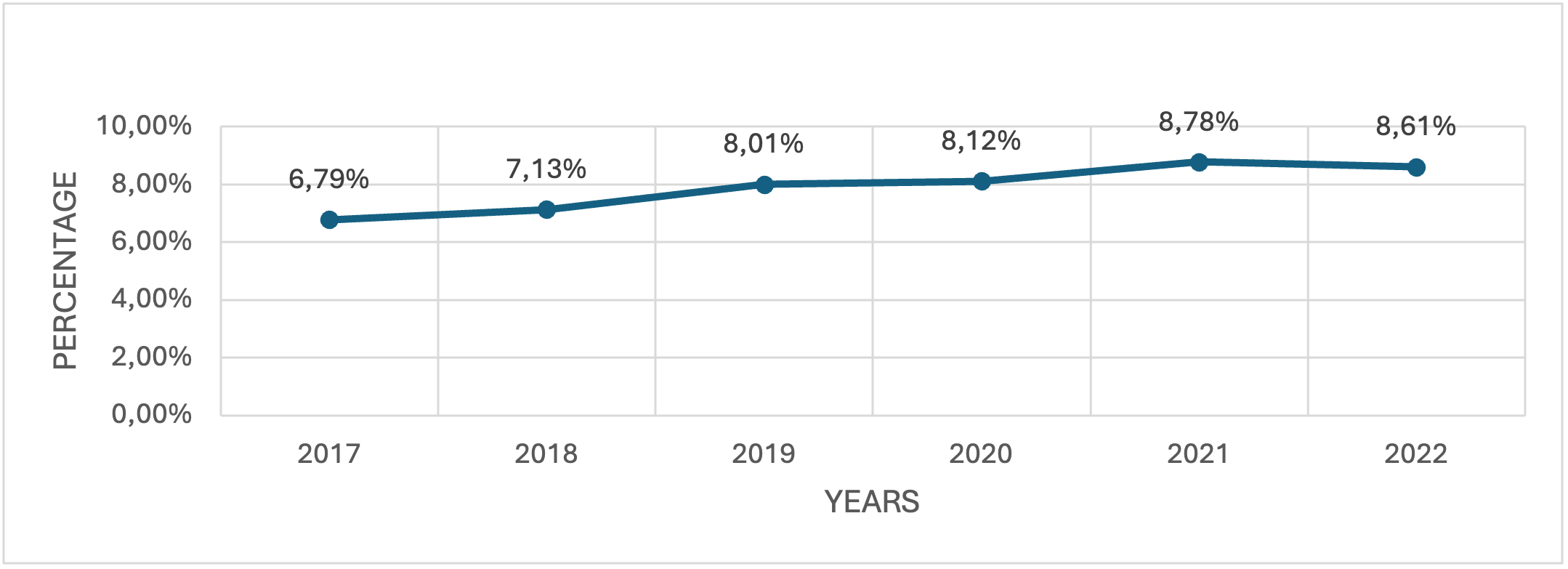

Digital services are likely to lower transaction costs in comparison to brick-and-mortar delivery. However, electronic services’ share to total services is even less than retail e-commerce’s share of retail sales, see Figures 3a and 3b. The data end in 2022 because of Service Annual Survey lag.

Figure 3a: Electronic Services revenue versus total services revenue

Figure 3b: Electronic services as a percentage of total services revenue[70]

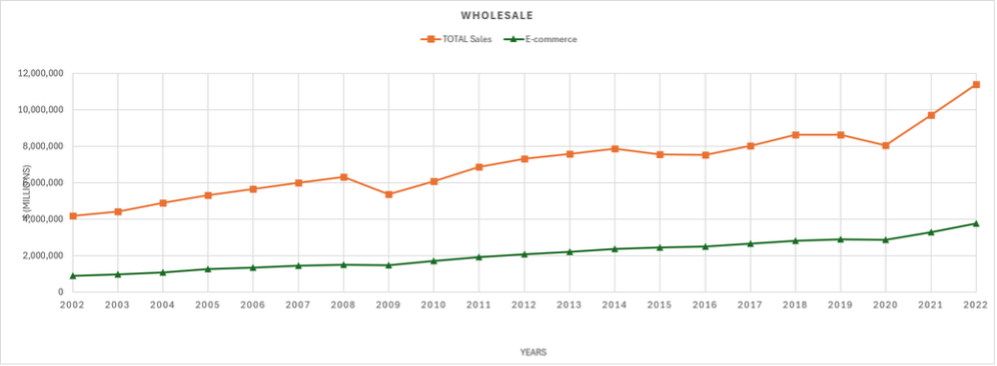

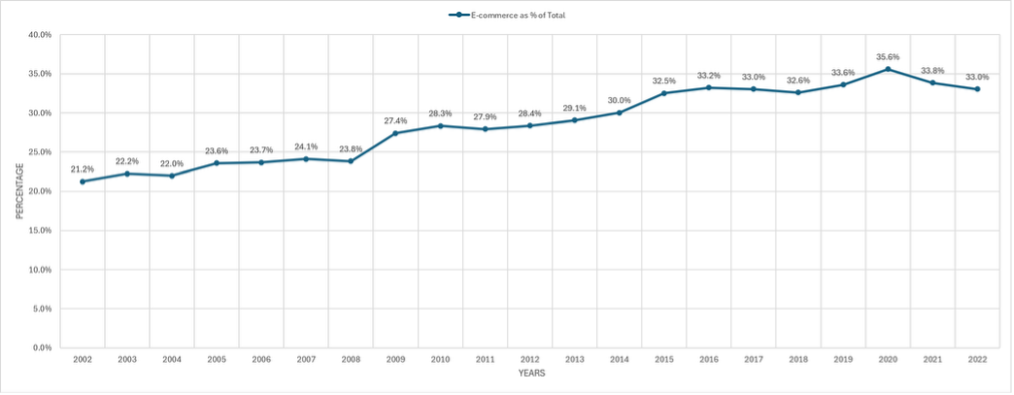

The wholesale e-commerce attained a much greater share of wholesale sales in comparison with retail e-commerce and electronic services, see Figures 4a and 4b. Firms face costs and benefits of internet access that differ from those for consumers. Net neutrality regulation likely will affect firms differently than consumers.

Figure 4a: Wholesale e-commerce sales versus total wholesale sales

Figure 4b: Wholesale e-commerce as a percentage of total wholesale sales[71]

- Conclusion

FCC net neutrality regulation was an anachronism. By classifying internet access as telecommunications, the FCC turned back the clock to the early days of telegraphy and voice telephone service. The FCC’s net neutrality approach did not recognize the internet as an information service, thus missing major innovations in software, computers, and communication.

There is perhaps nothing more Orwellian than the term net neutrality. Far from being neutral toward marketplace transactions, this policy tilted internet access regulation toward telecommunications and away from information services. The FCC’s final net neutrality ruling was a massive 512-page tome that imposed extensive regulations and yet was billed as “restoring Internet freedom.”[72]

Ohio Telecom will have long-term effects on the market for internet access, absent federal legislation or increases in state regulation. The FCC’s heavy-handed net neutrality approach diminished incentives to invest in internet access. Net neutrality regulation reduced product variety in internet access and increased transaction costs. Deregulation of the internet allows for increased investment in access and innovative transactions in the market for access.

The end of net neutrality regulation should generate economic benefits for consumers and firms. Lifting the regulatory burdens of net neutrality should increase competition, giving consumers and firms lower costs and more choices in internet access. This should improve consumer usage of the internet and stimulate the growth of retail e-commerce.

Daniel F. Spulber*

* Elinor Hobbs Professor of International Business, Professor of Strategy, Kellogg School of Management, Northwestern University, jems@kellogg.northwestern.edu.

I thank the editor Thibault Schrepel for helpful and constructive comments that improved the paper.

***

References

- [1] Ohio Telecom Association versus Federal Communications Commission (FCC), (hereafter Ohio Telecom, No. 24-3449 (6th Cir. 2025).

- [2] Ibid, at 4.

- [3] Ibid, at 4.

- [4] Ibid, at 2.

- [5] Ibid, at 3.

- [6] Ibid, at 3.

- [7] Ibid at 3.

- [8] Federal Communications Commission (FTC), In the Matter of Safeguarding and Securing the Open Internet, Restoring Internet Freedom” (hereafter net neutrality ruling), WC Docket No. 23-320, WC Docket No. 17-108, Declaratory Ruling, Order, Report and Order, and Order on Reconsideration, Adopted: April 25, 2024, Released: May 7, 2024. https://docs.fcc.gov/public/attachments/FCC-24-52A1.pdf, Federal Register, 89 Fed. Reg. 45,404 (May 22, 2024).

- [9] Daniel F. Spulber, 1989, Regulation and Markets, MIT Press, Chapter 2.

- [10] Ibid, Spulber at 71.

- [11] Ibid Spulber at 71. See also Heffron, F. A., with N. McFeely, 1983, The Administrative Regulatory Process, Longman, at 96 and Appendix II.

- [12] Spulber, 1989, supra note 9, at 72.

- [13] Spulber, 1989, supra note 9, at 72.

- [14] Chevron U.S.A., Inc. v. Natural Resources Defense Council, Inc., (hereafter Chevron), 467 U.S. 837, 843 (1984).

- [15] Ibid at 840.

- [16] Ibid at 842-843..

- [17] Ibid at 837.

- [18] Ibid at 844.

- [19] Ibid at 837.

- [20] National Cable & Telecommunications Association v. Brand X Internet Services, (hereafter Brand X), 545 U.S. 967 (2005).

- [21] Ibid, Scalia dissent, at 1017.

- [22] Ibid, Scalia dissent, at 1005.

- [23] Loper Bright Enterprises v. Gina Raimondo Secretary of Commerce, et al., (hereafter Loper Bright), 144 S. Ct. 2244 (2024) and Relentless, Inc., et al., Petitioners v. Department of Commerce, et al.

- [24] Ibid at 1.

- [25] Ibid at 35.

- [26] 47 U.S. Code § 153 – Definitions, (24).

- [27] Ohio Telecom, supra note 1 at.

- [28] Ohio Telecom, supra note 1 at 9.

- [29] Ohio Telecom, supra note 1 at 21

- [30] Bryant Veney, The Latest on Net Neutrality – Where Are We In 2026, BroadbandSearch, February 27, 2026, https://www.broadbandsearch.net/blog/net-neutrality.

- [31] Veney, ibid.

- [32] Veney, ibid.

- [33] Daniel F. Spulber and Christopher S. Yoo, Network Regulation: The Many Faces of Access, Journal of Competition Law and Economics, 1 (4), December, 2005, pp. 635-678.

- [34] FCC ruling, 2024, at 127. (“We retain the word “retail” in the definition of BIAS and hold that BIAS includes retail service provided by both facilities-based providers and resellers.”)

- [35] The FCC’s ruling applies section 224 of the Communications Act requiring “utilities to provide nondiscriminatory access to their poles, ducts, conduits, and rights-of-way to telecommunications carriers and cable television systems (collectively, attachers)”, at 224.

- [36] FCC ruling, 2024, at 82.

- [37] the FCC 2024 ruling states “Given otherwise existing authority that we retain under our open Internet rules and provisions of the Act from which we do not forbear, we find that there is no current federal need for those provisions—and, indeed, that they would conflict with the regulatory approach to BIAS that we find most appropriate,” at 247.

- [38] Spulber and Yoo, 2005, supra note 33.

- [39] Daniel F. Spulber and Christopher S. Yoo, Networks in Telecommunications: Economics and Law, (Cambridge University Press, 2009).

- [40] Matthew Lesh, 2022, Expanding the web: The case against net neutrality. No. 116. IEA Discussion Paper, https://iea.org.uk/wp-content/uploads/2022/12/Expanding-the-Web.pdf

- [41] Lesh, 2022, ibid.

- [42] Christian Hildebrandt and Lukas Wiewiorra. The past, present, and future of (net) neutrality: A state of knowledge review and research agenda, Journal of Information Technology 39, no. 1 (2024): 167-193.

- [43] Wolfgang Briglauer and Christopher Yoo, 2025, Efficiency and effectiveness of net neutrality rules in the mobile sector: Relevant developments and state of the empirical literature, Telecommunications Policy, 103111. At 13.

- [44] Shane Greenstein, Martin Peitz, and Tommaso Valletti. Net neutrality: A fast lane to understanding the trade-offs. Journal of Economic Perspectives 30, no. 2 (2016): 127-150.

- [45] Greenstein et al. ibid at 128.

- [46] Greenstein et al. ibid at 128.

- [47] Greenstein et al. ibid at 146-1447.

- [48] Barbara Van Schewick, 2007, Towards an economic framework for network neutrality regulation. Journal on Telecommunications and High Technology Law 5: 329-391, at 333.

- [49] Van Schewick, ibid. at 390.

- [50] Van Schewick, ibid. at 373.

- [51] David L. Bahnsen, What to Learn from the Worst Business Deal in History, July 18, 2025, Dividend Café, https://thebahnsengroup.com/dividend-cafe/what-to-learn-from-the-worst-business-deal-in-history-july-18-2025/

- [52] See George S. Ford, 2018, Regulation and Investment in the U.S. Telecommunications Industry, 50 Applied Economics. 6073, at 6082. See also George S. Ford, 2018. Net neutrality and investment in the US: A review of evidence from the 2018 restoring internet freedom order. Review of Network Economics, 17(3), pp.175-205.

- [53] Wolfgang Briglauer, Carlo Cambini, Klaus Gugler, and Volker Stocker, Net neutrality and high-speed broadband networks: evidence from OECD countries. European Journal of Law and Economics, 55, 533–571 (2023). https://doi.org/10.1007/s10657-022-09754-5.

- [54] Briglauer, et al., ibid, abstract at 533.

- [55] Briglauer, et al., ibid.

- [56] Adam D. Rennhoff and James Bakuli, The Effect of Net Neutrality Rules on the Cost and Availability of High-Speed Internet Service to Urban and Rural Consumers, abstract at 1. Available at SSRN: https://ssrn.com/abstract=4415299 or http://dx.doi.org/10.2139/ssrn.4415299

- [57] Rennhoff and Bakuli, ibid abstract at1.

- [58] The American Society of Civil Engineers, A Comprehensive Assessment of America’s Infrastructure, 2025 Infrastructure Report Card, (hereafter 2025 Report Card), at 37. https://infrastructurereportcard.org/cat-item/broadband-infrastructure/.

- [59] 2025 Report Card, ibid. at 36.

- [60] Wallsten, Scott, and Stephanie Hausladen, 2009, Net neutrality, unbundling, and their effects on international investment in next-generation networks. Review of Network Economics 8, no. 1: 90-112.

- [61] Wallsten and Hausladen, ibid at 91.

- [62] Wallsten and Hausladen, ibid at 102.

- [63] Wallsten and Hausladen, ibid at 102.

- [64] Goldfarb, Avi, and Catherine Tucker. “Digital economics.” Journal of economic literature 57, no. 1 (2019): 3-43.

- [65] Wheaton, William C. and Tung, Edward, Bricks or Clicks? The Efficiency of Alternative Retail Channels (February 3, 2019). MIT Center for Real Estate Research Paper No. 9, https://ssrn.com/abstract=3406046 or http://dx.doi.org/10.2139/ssrn.3406046

- [66] Halibas, A. S., Van Nguyen, A. T., Akbari, M., Akram, U., & Hoang, M. D. T. 2023. Developing trends in showrooming, webrooming, and omnichannel shopping behaviors: Performance analysis, conceptual mapping, and future directions. Journal of Consumer Behaviour, 22(5), 1237–1264. https://doi.org/10.1002/cb.2186; Brynjolfsson, E., Hu, Y. J., & Rahman, M. S. 2013. Competing in the age of omnichannel retailing. MIT Sloan Management Review, 54(4), 23–29. Brynjolfsson, E., & Smith, M. D. (2000). Frictionless commerce? A comparison of internet and conventional retailers. Management Science, 46(4),563–585. https://doi.org/10.1287/mnsc.46.4.563.12061

- [67] FCC, net neutrality ruling, ibid at 183.

- [68] Source for Figures 1a and 1b: The data for the years 1999 is from: “Estimated Annual U.S. Retail Trade Employer-only Sales – Total and E-commerce: 1998-2022,” “[e]stimates are shown in millions of dollars and are based on data from the Annual Retail Trade Survey. Estimates have been adjusted using final results of the 2017 Economic Census.]” U.S. Census Bureau, *New* Annual Retail Trade Survey: 2022 (restated), September 25, 2024, Table: U.S. Retail Trade Sales – Total and E-commerce (1998-2022), https://www.census.gov/data/tables/2022/econ/arts/2022restated/annual-report.html, accessed February 4, 2026. The data for years 2000 to 2025 (Q1 to Q3) is generated by adding up the quarterly time series data from the excel: “[e]stimated Quarterly U.S. Retail Sales (Adjusted): Total and E-commerce,” “(Estimates are based on data from the Monthly Retail Trade Survey and administrative records.)” U.S. Census Bureau, Quarterly Retail E-Commerce Sales, March 10, 2026, Table: Time Series Tables https://www.census.gov/retail/ecommerce.html, accessed February 4, 2026.

- [69] Source: Amazon annual reports, 1999-2024, and quarterly reports, 2025, https://ir.aboutamazon.com/sec-filings/default.aspx.

- [70] Source for Figures 3a and 3b. “Table 9. Estimated Revenue from Electronic Sources for Employer Firms: 2015 Through 2022”, “[Estimates are based on data from the 2022 Service Annual Survey and administrative data and incorporate the 2017 North American Industry Classification System (NAICS) changes. Dollar volume estimates are published in millions of dollars, unit estimates are published in thousands of units; consequently, results may not be additive. Estimates have been adjusted using results of the 2017 Economic Census where applicable. In some instances, results from the 2017 Economic Census may reflect revisions based on additional analytical review following the release of the 2017 Geographic Area Statistics.]”, U.S. Census Bureau, Service Annual Survey Latest Data (NAICS-basis) 2022, September 25, 2024, Table 9. Estimated Revenue from Electronic Sources for Employer Firms: 2015 Through 2022, https://www.census.gov/data/tables/2022/econ/services/sas-naics.html , Accessed March 3, 2026.

- [71] Source for Figures 4a and 4b: The data for the Total Wholesale is taken from the excel: “Table 1. Estimated Sales of U.S. Merchant Wholesalers: 1992 through 2022.” “[Sales estimates are shown in millions of dollars and are based on data from the Annual Wholesale Trade Survey. Estimates have been adjusted using results of the 2017 Economic Census]”, U.S. Census Bureau, Annual Report for Wholesale Trade: 2022, January 16, 2024, Table 1. Estimated Sales of U.S. Merchant Wholesalers: 1992 through 2022 https://www.census.gov/data/tables/2022/econ/awts/annual-reports.html, accessed February 4, 2026. The data for the Ecommerce Wholesale is taken from the excel: “Table 2. Estimated E-Commerce Sales of U.S. Merchant Wholesalers: 1998 through 2022,”“[E-Commerce sales estimates are shown in millions of dollars and are based on data from the Annual Wholesale Trade Survey. Estimates have been adjusted using results of the 2017 Economic Census]” U.S. Census Bureau, Annual Report for Wholesale Trade: 2022, January 16, 2024, Table 2. Estimated E-Commerce Sales of U.S. Merchant Wholesalers: 1998 through 2022 https://www.census.gov/data/tables/2022/econ/awts/annual-reports.html, accessed February 4, 2026.

- [72] Net neutrality ruling, 2024.